2,588

TCPA lawsuits filed in an 11-month period in 2025, many targeting insurance agencies using automated outreach. [S-Henson26]

Third-party citation

For Independent Insurance Agency Principals

COI requests eat your mornings. Thirty renewals are due this month and nobody has touched the prep. Your best CSR is two bad weeks from burning out. We put AI on the high-volume work, with a licensed agent approving every output before it goes out and a full audit trail if anyone ever asks.

Insurance is one of the industries where we've gone especially deep. All About AI also builds custom AI systems for other operationally complex businesses.

Fixed-fee diagnostic. Written scope before any build begins.

Independent agencies · Commercial and personal lines · E&O audit trail by design · Human approval on every client communication

Illustrative, not a client result. Shows the governance model: AI drafts, licensed agent approves, everything is timestamped.

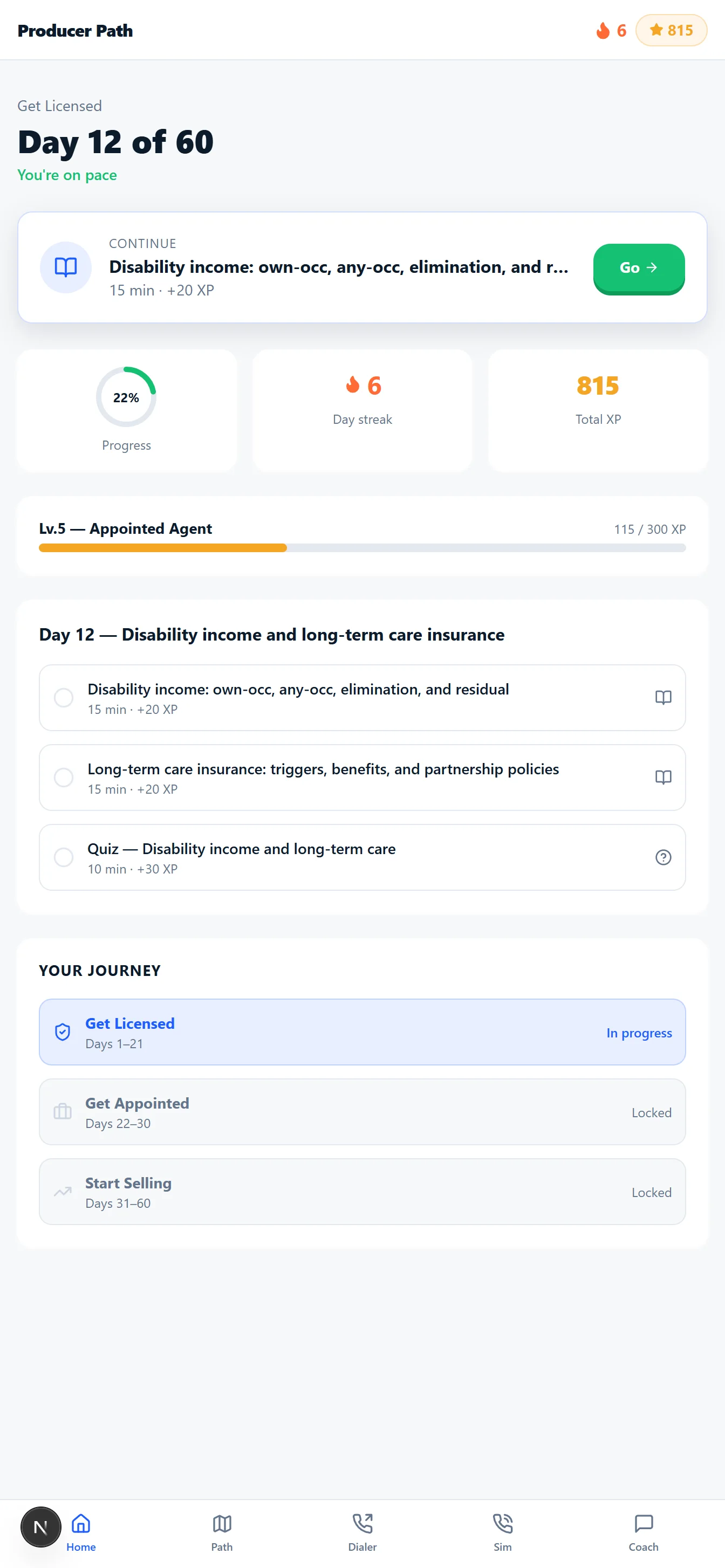

Producer Path is a gamified 60-day training portal that takes a brand-new producer from unlicensed to selling: licensing exam prep, appointment and compliance steps, then live sales-call practice against AI prospects that actually talk back.

Start small, grow from there. Producer Path is the fastest way to work with us: no systems integration, no IT project, your new producers just get a path. When you're ready to hand the paperwork to AI too, the Oversight Layer™ is the next step. Same partner, bigger lift.

Real product screenshot. Demo account data shown.

Step through the workflow. Every beat is simulated demo data. The governance model is real.

2:44 PM · Inbound email, simulated

The CSR is on a renewal call. The email sits in the queue. Without the Approval Inbox, she handles this when she gets off the call, squeezing 15 minutes of AMS work into the gap before the next task. With the Approval Inbox, the next beat happens automatically.

FROM: sarah@mapleridgeconstruction.com TO: certs@rivervalleyins.com SUBJECT: COI needed -- named additional insured Hi, we need a certificate of insurance for our GC on the Harbor St project. They need to be named as additional insured. Deadline is 5 PM. Certificate holder: Arbor Group LLC 411 Harbor St, Suite 200 Columbus, OH 43215 Thanks Sarah Chen

SIMULATED DEMO DATA. Illustrative workflow only. Not a client result.

2:44 PM + 19 seconds · AI action, no human yet

AI read the email, identified the insured, pulled the matching GL policy from the AMS, and drafted the ACORD 25 with the correct certificate holder and additional insured language. It placed the draft in the approval inbox with a plain-English flag. Nothing has left the agency yet.

AI ACTION LOG (simulated)

--------------------------

Request type: COI -- standard additional insured

Policy located: Maple Ridge Construction, LLC

Policy No: GL-2024-88821 (simulated)

Carrier: Hartwell Mutual (simulated)

Coverage: Commercial General Liability

Limits: $1M / $2M

Status: Active, exp. 04/01/2027

Certificate holder populated:

Arbor Group LLC

411 Harbor St, Suite 200

Columbus, OH 43215

Additional insured wording: matched to

policy endorsement language on file.

Draft placed in: APPROVAL INBOX

Flag: Standard COI. Verify AI wording

matches policy endorsement.

Human action required before send: YES

SIMULATED DEMO DATA. Illustrative workflow only. Not a client result.

2:47 PM · Licensed agent action

The agent opens the inbox between calls. Three checks. Thirty seconds. Click Approve below to see what happens.

APPROVAL INBOX (simulated) -------------------------- Draft: Maple Ridge COI -- Arbor Group AI Flag: Verify additional insured wording Status: PENDING REVIEW Agent review: Policy number: confirmed Cert holder: confirmed AI wording: matches endorsement on file Coverage dates: confirmed active

Agent: M. Torres, CIC (simulated) · Time: 2:47 PM

SIMULATED DEMO DATA. Illustrative workflow only. Not a client result.

2:47 PM + 4 seconds · Certificate sent and E&O trail written

The audit log writes itself. Request received, AI drafted, agent reviewed, agent approved, cert delivered. Every field timestamped. If an E&O claim ever cites this certificate, the agency has a contemporaneous chain of custody showing a licensed professional reviewed and approved before it went out. That record does not exist in a system without a governance layer.

SIMULATED DEMO DATA. Illustrative workflow only. Not a client result.

Every cert. Every time. Same day.

This is the COI workflow. Same architecture handles renewal outreach, coverage follow-ups, and every other client-facing output your agency sends. One approval layer. One audit trail. Everything documented.

SIMULATED DEMO DATA. Illustrative workflow only. Not a client result.

Demo above is simulated. All names, policy numbers, and carrier references are fictional and illustrative only. No real client or agency data is shown.

The free E&O Exposure Scorecard takes 10 minutes. It maps the governance gaps in your current workflows and gives you a plain-English picture of where your agency is most exposed right now.

No commitment. Takes 10 minutes.

Open your CSR's inbox on any Monday morning: six COI requests before 9am, each one taking 15 minutes to pull, draft, and send. That is the renewal prep she planned for this week. It won't happen. You have 30 accounts renewing this month and half of them haven't been touched.

Meanwhile, every AI-drafted email your team sends without a documented review is an undocumented coverage representation. Your E&O carrier may not defend it. Independent agencies are also in the crosshairs of a growing TCPA lawsuit wave: 2,588 TCPA suits filed in an 11-month window in 2025, many targeting agencies running automated client outreach. [S-Henson26] Texas SB 140 (effective September 1, 2025) added a private right of action at up to $5,000 per violation. Twelve or more states have followed. [S-iDudes26]

The agencies that come out ahead automate the repetitive work AND keep a licensed agent in the approval loop on every client-facing output. Both. Every time.

"My CSRs spend half their day on COIs. That's not what I pay them for."

"I worry about what our system sends automatically. Was that reviewed by anyone licensed?"

"Renewal season is chaos. We miss accounts because nobody flagged them."

"I can't afford to add headcount, but the volume keeps growing."

2,588

TCPA lawsuits filed in an 11-month period in 2025, many targeting insurance agencies using automated outreach. [S-Henson26]

Third-party citation

65%

Reduction in E&O exposure reported in vendor analysis of AI-assisted policy comparison and gap detection. [S-ISW26]

Third-party vendor claim, validate live

79%

Labor cost reduction on policy intake, from 12 minutes to 2.5 minutes per form, reported in an agency AI workflow case study. [S-Perspective26]

Third-party vendor case study (Perspective AI, 2026)

Statistics are third-party citations, not All About AI client results. Validate against your agency's data. No guarantee of results.

Five workflows take your agency's highest-volume back-office work off your team's plate: COIs, AMS intake, renewal triage, client communications, and FNOL. A licensed agent approves every output before it goes out, and everything it touches lands in a full E&O audit trail.

Standard COI requests are handled by AI: it reads the request, pulls the policy from your AMS, drafts the certificate with the correct certificate holder details, and places the draft in the agent's approval inbox. The agent reviews and approves in seconds. Non-standard or complex certificates go to a human queue, not guessed at. Every COI issued carries a timestamped audit entry: request received, AI draft generated, agent approved, document sent.

✓ AMS integration (Applied Epic, AMS360) · Standard: instant queue, complex: human handling · Every issuance timestamped in the E&O log

The Approval Inbox demo above shows this workflow in real time.

ACORD forms, carrier documents, and endorsement papers that arrive as PDFs are read by AI, structured into the correct AMS fields, and placed in a review queue. Your CSR confirms before anything writes to the system. Discrepancies and ambiguous fields are flagged for human review. The AI never writes to your AMS without a person confirming the extraction is accurate. Industry case study data reports 79% labor reduction on this workflow, from 12 minutes to 2.5 minutes per form. [S-Perspective26] (Perspective AI, 2026. Third-party case study, not an All About AI client result.)

✓ ACORD forms plus carrier docs · Structured extraction, CSR confirms, then AMS write · Discrepancies flagged, never guessed

The system works your renewal pipeline 90 to 120 days out. It pulls the renewal list from your AMS, flags at-risk accounts based on premium change, loss ratio, or policy-gap signals, assembles the relevant policy data for remarketing comparison, and builds the renewal prep package for your producer. A third-party case study found a regional brokerage using AI renewal triage identified 287 at-risk accounts and achieved a 9-point retention lift on its commercial book. (Perspective AI, 2026. [S-Perspective26] Not an All About AI client result.) Your producer still makes every coverage recommendation and client call. The AI handles the data assembly so that call actually happens.

✓ 90 to 120 day pipeline · At-risk account flagging · Remarketing package assembly · Agent makes every coverage decision

Any AI-drafted client communication (renewal outreach, coverage change follow-up, claim status update) goes into an approval inbox before it reaches the client. A licensed agent reviews the draft, edits if needed, and approves. The audit log records: AI draft created, agent reviewed, agent approved or edited, message sent, timestamp. That record is your E&O documentation. Consent and opt-out mechanics for outbound communications are built into the workflow by design, not added as an afterthought. [Not legal advice. Coordinate with counsel for your state-specific requirements.]

✓ No client communication sends without licensed-agent approval · Full audit entry on every message · Consent architecture built in

First Notice of Loss calls and emails: the AI reads the intake, structures the claim information, and routes it to the correct handler with context attached. Urgent or complex claims go to a licensed team member immediately. Coverage determinations and reserve guidance stay in human hands, always.

✓ FNOL data extraction · Handler routing · Coverage determination is always human

In insurance, every AI-generated communication that reaches a client without a documented review is a potential E&O event. The Oversight Layer™ is the architecture that prevents that. It is not a feature bolted on after the fact.

Every AI action: every draft, every review, every approval, every send is timestamped and logged. If an E&O claim arises, you have a contemporaneous record showing a licensed agent reviewed and approved every client-facing output before it went out. That record does not exist if you are using a tool with no governance layer.

TCPA lawsuit volume against insurance agencies is substantial and growing, with 12 or more states adding mini-TCPA laws with private rights of action (Texas SB 140: up to $5,000 per violation, effective September 1, 2025). [S-iDudes26] Our implementation builds consent documentation and opt-out mechanics into the client communication workflow as a condition of every outbound message, not a bolt-on. [Not legal advice. Requirements vary by state. Coordinate with counsel.]

The AI drafts and assembles. It never makes coverage decisions, recommends specific carriers, or represents coverage terms to clients on its own. Every coverage-related output is reviewed and approved by a licensed professional before it leaves the agency.

If a payer changes requirements, a state law shifts, or you simply want to review before re-enabling, pause the AI in one click. Your operations continue manually while you investigate. The AI is infrastructure you control completely, not a dependency you can't turn off.

The system runs on your existing AMS (Applied Epic, AMS360). We do not replace your stack or ask you to migrate to a new platform. AI workflows are configured to your agency's specific products, carriers, and communication standards, approved by your team before anything goes live. We do not train on your client data.

Tools that automate without a governance layer give you efficiency today and an undocumented E&O exposure tomorrow. The question is not whether to use AI in your agency. It is whether the AI you use is supervised by a licensed professional every single time it touches a client.

Three phases. The only thing you commit to first is the Assessment. Every implementation begins there: scoped, priced, and in writing before any build begins.

We map your agency's back-office workflows: COI volume, AMS data entry time, renewal prep hours, CSR communication load. We identify where AI can safely do the work, flag the E&O and TCPA exposure points in your current process, and deliver a written scope with a fixed implementation price. You see the full picture before committing to a build. This document is itself useful: a map of your operational risk exposure and the opportunity to close it.

We configure the AI workflows, wire in the approval inbox, install the audit log, and set up the E&O documentation trail. Every workflow template is reviewed and approved by your licensed team before activation. We integrate with your AMS and test against your actual policy types and carrier documents. You review everything before the system goes live with clients. Scope is confirmed after the Assessment. Price above is indicative.

The system runs. Your team works from the approval inbox. The audit log captures every action. We handle maintenance, adapt to AMS updates and carrier changes, and monitor for drift. When new state mini-TCPA laws pass or your AMS vendor pushes a major update, we handle the compliance adaptation. Renewal season surge support is included.

Renewal triage: AI surfaces the accounts, assembles the prep, and puts your producer on the call that saves the relationship.

Note: Illustrative workflow, not a documented client result. Shown to demonstrate the governance model only.

This is built for you if…

This is NOT for you if…

Start with a free fit call.

Fixed-fee diagnostic. We map your workflows, identify the governance gaps, and deliver a written scope with a fixed implementation price. You see everything before any build begins.

Agency Ops & E&O Exposure Assessment. Scope and price confirmed in writing before any implementation begins.

Compliance & Disclosures

No guarantee of results: Statistics on this page are third-party citations, not All About AI client results. The 79% labor reduction figure and the 9-point retention lift and 287 at-risk accounts identified are from a third-party vendor case study (Perspective AI, 2026); the 65% E&O exposure reduction figure is from a third-party vendor analysis. Your actual results depend on your agency's workflow volume, AMS setup, carrier mix, and team. We do not guarantee specific labor savings, retention outcomes, or compliance results.

E&O note: The audit trail and approval workflow described are designed to support defensibility in an E&O context. They are not a guarantee of E&O coverage, a substitute for professional liability insurance, or legal advice on what constitutes adequate documentation under your specific E&O carrier's requirements. Coordinate with your E&O carrier and licensed counsel.

TCPA note: TCPA lawsuit exposure for insurance agencies using automated outreach is documented and substantial. Our implementation builds consent and opt-out architecture into client communication workflows. We do not assert any specific TCPA rule or regulation as current law. Requirements change, vary by state, and should be confirmed with licensed telecommunications and insurance counsel before any automated outreach program is deployed. References to TCPA lawsuit volume are from third-party legal sources. [S-Henson26][S-iDudes26]

Coverage decisions: Nothing in this system makes coverage recommendations, interprets policy terms for clients, or advises on coverage gaps. The AI drafts and routes; licensed agents review and approve all client-facing communications.

Data handling: Client and policyholder data is handled under a data processing agreement provided at onboarding. We do not train AI models on your client data. Data stays within your AMS and authorized integration points.

Regulatory references are for context only and do not constitute legal advice. Requirements vary by state, agency type, and carrier. Sources: [S-Henson26] Henson Legal AI Voice Compliance 2026; [S-iDudes26] iDudes Mini-TCPA State Laws Insurance Agents 2026; [S-ISW26] InsuranceSupportWorld AI Broker Guide; [S-Perspective26] Perspective AI Insurance Agencies 2026 (case study data).